Last updated: June 2026 By Editorial Team , UAE business formation specialists with direct experience in DIFC, free zone, and VARA licensing processes.

Last updated: June 2026

By Editorial Team, UAE business formation specialists with direct experience in DIFC, free zone, and VARA licensing processes. Full bio →

Table of Contents

What Is a Fintech Company in Dubai and Why the UAE Is the Right Market

Regulatory Pathways: DFSA License vs Standard Professional License

The DIFC FinTech Hive and Innovation Testing License for Early-Stage Fintechs

VARA Licensing for Crypto and Blockchain Fintech in Dubai

Fintech Company Setup Costs: Regulated vs Non-Regulated

How to Start a Fintech Company in Dubai: Step-by-Step Process

Key Takeaways and Next Steps

References

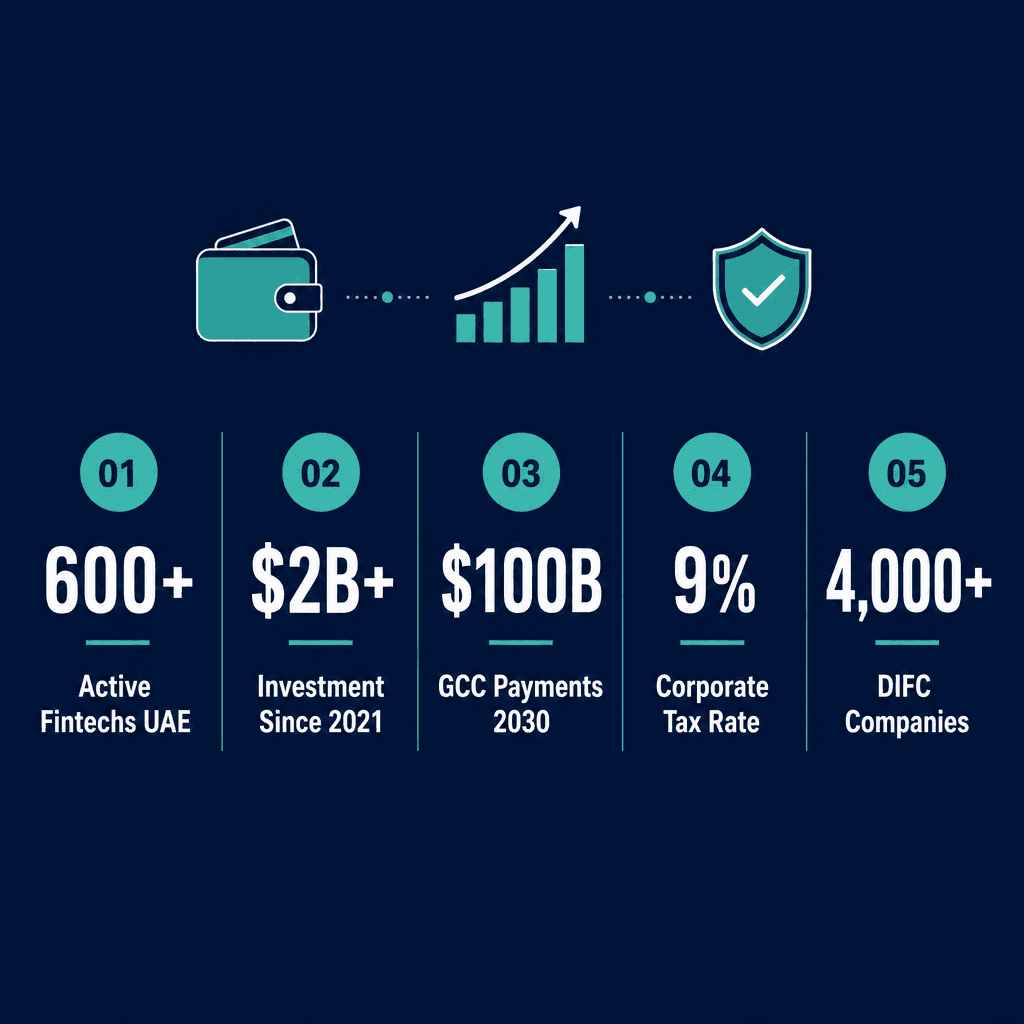

Dubai ranks among the top 10 global fintech hubs by deal volume in 2026, with the UAE fintech sector attracting over $2 billion in cumulative investment since 2021 (UAE Fintech Report, 2024). The UAE has over 600 active fintech companies as of 2024. The GCC digital payments market is projected to exceed $100 billion by 2030 (RedSeer Consulting, 2023). The DIFC alone houses over 4,000 registered companies, including 120+ fintech firms. Dubai's Virtual Assets Law No. 4 of 2022 established VARA as an independent regulatory authority, making it one of the first jurisdictions globally to create a dedicated crypto regulator. And the UAE Corporate Tax rate sits at 9% on income above AED 375,000, with 0% applying to qualifying free zone entities on qualifying income (Federal Tax Authority, 2023).

Dubai has deliberately positioned itself as a global fintech hub. The DIFC FinTech Hive accelerator, ADGM's regulatory sandbox, and the Dubai Financial Services Authority's (DFSA) progressive licensing framework together form one of the most structured and accessible fintech ecosystems in the world. For founders based in the US or anywhere else, the entry points are clearer than you might expect.

This guide covers everything you need to start a fintech company in Dubai: the types of fintech businesses you can form, the two main regulatory pathways, what activities require a DFSA or CBUAE license versus a standard professional license, the DIFC FinTech Hive accelerator, VARA licensing for crypto, realistic setup costs, and a clear step-by-step process to get your company operational.

What Is a Fintech Company in Dubai and Why the UAE Is the Right Market

A fintech company in Dubai is a technology-driven business providing financial services, from payments and lending to crypto and insurtech, within the UAE's dual regulatory framework. Dubai offers founders a progressive licensing environment, tax-free profits on qualifying free zone income, and direct access to the $3.5 trillion GCC financial services market. If you want to start a fintech company in Dubai, the first question is what type of fintech you're building.

Types of Fintech Businesses You Can Set Up in Dubai

The UAE supports a wide range of fintech business models. Here's what you can set up:

Payment processing and digital wallets

Peer-to-peer and digital lending platforms

Wealth management and robo-advisory services

Insurtech and embedded insurance products

Crypto, blockchain, and tokenisation businesses

Open banking API providers and data aggregators

B2B financial software, KYC/AML tools, and compliance SaaS

Remittance and cross-border payment services

Tabby, the UAE-based buy-now-pay-later (BNPL) platform, launched its fintech license in Dubai and scaled to over 4 million users across the GCC. That growth trajectory illustrates the market scale available to founders who set up here early and correctly.

Why Dubai Attracts Global Fintech Founders

0% corporate tax on qualifying free zone income

100% foreign ownership permitted in free zones

DIFC FinTech Hive and ADGM regulatory sandbox offer structured early-stage pathways

Strategic time zone bridging Asia, Europe, and Africa

Large unbanked and underbanked population across MENA as an addressable market

Stripe launched its MENA operations from the DIFC, citing the DFSA's progressive licensing framework and access to regional banking infrastructure as primary factors. For non-regulated fintech founders, those building B2B software, open banking tools, or SaaS infrastructure, start your tech business at Dubai South Business Hub Free Zone for a lower-cost alternative to DIFC's premium positioning.

Regulatory Pathways: DFSA License vs Standard Professional License

Fintech companies in Dubai operate under two main regulatory pathways: a DFSA license (required for regulated financial activities inside the DIFC) or a standard UAE trade or professional license (sufficient for software, SaaS, and non-regulated fintech). Choosing the wrong pathway is the most common and costly mistake founders make when pursuing fintech business setup in the UAE.

DFSA Licensed Fintech vs Standard Professional License: Key Differences

Feature | DFSA Licensed (DIFC) | Standard Professional License |

|---|---|---|

Setup Timeline | 3–12 months | 3–7 working days |

License / Application Fee | AED 10,000–50,000+ | AED 12,000–20,000/year |

Minimum Capital Requirement | AED 500,000–10,000,000+ | ❌ None required |

Can Hold Client Funds | ✅ Yes | ❌ No |

Suitable For | PSPs, lenders, investment advisors | SaaS, APIs, KYC tools, B2B software |

Annual Supervision Fee | AED 25,000–100,000+ | ❌ Not applicable |

Foreign Ownership | ✅ 100% | ✅ 100% |

Activities That Require a DFSA or CBUAE License

Some fintech activities are regulated by law. You'll need a DFSA or CBUAE license if your business involves:

Accepting deposits or holding client funds

Operating a payment service provider (PSP) or electronic money institution (EMI)

Providing regulated investment advice or portfolio management

Operating a peer-to-peer lending platform

Issuing insurance products (requires Insurance Authority license)

A founder building a digital remittance app, following the model used by Lulu Exchange or Al Ansari Exchange, must obtain a CBUAE Payment Service Provider license, not a simple trade license. The CBUAE issued its Payment Services Regulation in 2021, creating a tiered licensing framework with five categories (centralbank.ae, 2021). Over 600 firms are currently authorised by the DFSA within the DIFC.

Activities That Operate Under a Standard Professional License

Not every fintech needs a regulated license. A professional business license in Dubai is sufficient for:

B2B financial software development and white-label platforms

Open banking API providers and data aggregators

Fintech SaaS tools (compliance, KYC, AML software)

Financial education and comparison platforms

Backend infrastructure for banks and insurers

A company building KYC-as-a-Service software for UAE banks, similar to what Jumio or Onfido do globally, does not hold client funds and qualifies for a professional license at a free zone rather than a DFSA-regulated entity. Professional license setup at Dubai free zones typically starts from AED 12,000–18,000 per year, making it the practical first choice for non-regulated fintech founders.

The DIFC FinTech Hive and Innovation Testing License for Early-Stage Fintechs

The DIFC FinTech Hive is the largest fintech accelerator in the Middle East, Africa, and South Asia. It offers early-stage startups mentorship, investor access, and a path to the DFSA Innovation Testing License, a time-limited regulatory sandbox that lets you test regulated financial products before obtaining a full license. If you're figuring out how to launch a fintech startup in Dubai at the pre-revenue stage, this is the most structured route available.

How the DIFC FinTech Hive Accelerator Works

Annual cohort-based programme with mentorship from 50+ global financial institutions

Access to DIFC's network of banks, insurers, and asset managers as potential clients

No equity taken, FinTech Hive does not take a stake in your company

Graduates include fintechs that raised Series A funding and expanded regionally

Sarwa, the UAE's first robo-advisory platform, participated in the DIFC FinTech Hive programme and subsequently obtained a DFSA license. It now manages assets for over 80,000 clients across the UAE. The programme has supported over 300 startups since its launch in 2017 (fintechhive.difc.ae, 2024).

The DFSA Innovation Testing License Explained

The DFSA Innovation Testing License, introduced in 2017, was one of the first regulatory sandbox frameworks in the region (dfsa.ae, 2017, still accurate as of 2026). Here's what it covers:

Lets you test regulated financial services with real customers under a restricted license

Time-limited, typically two years, with defined client and transaction limits

Reduces the cost and complexity of full DFSA authorisation before product-market fit

Applicants must demonstrate a genuine innovation that can't be tested under existing authorisation

A cross-border B2B payments startup can use the Innovation Testing License to run live pilots with up to 50 corporate clients before committing to the full DFSA authorisation process and its associated capital requirements. That's a meaningful risk reduction for any early-stage team.

VARA Licensing for Crypto and Blockchain Fintech in Dubai

The Virtual Assets Regulatory Authority (VARA) is Dubai's dedicated regulator for crypto and blockchain businesses. Any company offering virtual asset services, trading, custody, exchange, issuance, or transfer, must obtain a VARA license. This is separate from the DFSA framework and applies across all of Dubai, excluding the ADGM jurisdiction. For anyone pursuing fintech company formation in the UAE's crypto sector, VARA is the authority you're dealing with.

Who Needs a VARA License and What It Covers

You'll need a VARA license if your business involves:

Virtual asset exchanges and trading platforms

Crypto custody and wallet service providers

Token issuance and initial exchange offerings (IEOs)

Virtual asset transfer and settlement services

Crypto broker-dealers and advisory firms

Bybit, one of the world's largest crypto exchanges, obtained a VARA license in Dubai in 2023, one of the first major global exchanges to be fully licensed in the emirate. That signals VARA's credibility with institutional-grade operators. Dubai's Virtual Assets Law (Law No. 4 of 2022) established VARA as an independent regulatory authority, giving it a clear legal mandate that's rare globally.

VARA License Categories and Estimated Costs

VARA issues licenses across four stages: Preparatory, Operational (MVP), Operational (Market Product), and full Operational License

Application fees range from AED 40,000 to AED 200,000+ depending on activity category (vara.ae, 2024)

Exchange operators face higher minimum capital thresholds than advisory firms

VARA requires a physical presence in Dubai, a registered office address is mandatory

Full operational license annual fees start from AED 40,000 for advisory activities (vara.ae, 2024)

Worth flagging: a crypto and blockchain business setup in Dubai that only develops non-custodial wallet software, where users control their own private keys, may operate under a professional license rather than a VARA-regulated license. That's a significant cost and complexity difference, so getting the classification right before you apply matters.

Is a VARA license required for all blockchain businesses in Dubai?

No. VARA licensing applies to businesses that provide virtual asset services to clients, including trading, custody, exchange, and transfer. Pure blockchain software developers, non-custodial wallet builders, and infrastructure providers who do not hold client assets or facilitate transactions on their clients' behalf typically qualify for a standard professional license instead.

Fintech Company Setup Costs: Regulated vs Non-Regulated

Setting up a non-regulated fintech company in Dubai costs AED 12,000–25,000 per year for a professional license at a free zone. A regulated DFSA-licensed fintech requires AED 50,000–150,000+ in licensing fees alone, plus minimum capital requirements that can reach AED 1 million or more. Understanding this cost gap is essential for fintech business setup planning in the UAE.

Cost Breakdown for a Non-Regulated Fintech (Professional License)

Free zone license fee: AED 12,000–20,000 per year depending on the zone

Visa allocation: typically 1–3 visas included in entry-level packages

Office / flexi-desk: AED 5,000–15,000 per year for shared workspace

Company registration and government fees: AED 3,000–5,000 one-time

Bank account setup: no fee, but most UAE banks require minimum deposits

A B2B fintech SaaS startup building compliance automation tools can set up at Dubai South Business Hub Free Zone under a professional license for well under AED 30,000 in year one, a fraction of the cost of a DFSA-regulated entity. Calculate your fintech company setup cost to model your exact budget before committing.

Cost Breakdown for a Regulated Fintech (DFSA or CBUAE License)

DFSA application fee: AED 10,000–50,000 depending on license category

DFSA annual supervision fee: AED 25,000–100,000+ based on activity and revenue

Minimum capital requirement: AED 500,000–10,000,000+ depending on activity

DIFC establishment fee and registered office: AED 10,000–30,000 per year

Legal and compliance advisory for DFSA application: AED 50,000–150,000

A regulated payment institution seeking a CBUAE PSP license (Category B) must maintain minimum paid-up capital of AED 3,000,000 (centralbank.ae, 2021). A DFSA Category 3C investment firm faces a minimum capital threshold of USD 500,000 (dfsa.ae, 2024). These figures separate serious operators from early-stage startups who should explore the Innovation Testing License first. For non-regulated founders, launch your company at Dubai South Business Hub Free Zone to keep year-one costs predictable.

How to Start a Fintech Company in Dubai: Step-by-Step Process

To start a fintech company in Dubai, you must first determine whether your activity is regulated or non-regulated, choose the correct jurisdiction and license type, prepare your documentation, submit your application, open a corporate bank account, and obtain your visa. The full process takes 2–8 weeks for non-regulated setups and 3–12 months for regulated ones. Here's how to launch your fintech startup in Dubai without wasting time on the wrong pathway.

A four-step process timeline showing how to start a fintech company in Dubai, from determining regulatory category to activating operations. How to Start a Fintech Company in Dubai References

Editorial sources available on request. Full citation list is being compiled.