Last updated: June 2026 By Editorial Team , Business setup specialists covering UAE free zone formation, banking compliance, and corporate structuring since 2018.

Last updated: June 2026

By Editorial Team, Business setup specialists covering UAE free zone formation, banking compliance, and corporate structuring since 2018. Full bio →

Table of Contents

What Is Free Zone Company Structure for Easy Bank Account Opening in UAE and Why It Matters

Which Free Zone You Choose Determines Whether the Bank Says Yes

Seven Structural Decisions That Make UAE Bank Account Opening Straightforward

Free Zone Office Solutions and How They Affect Your Bank Application

Shareholder Profile and Business Activity: The Two Factors Banks Scrutinise Most

Match Your Bank to Your Free Zone for Faster Approval

Structure First, Then Apply

Key Takeaways

References

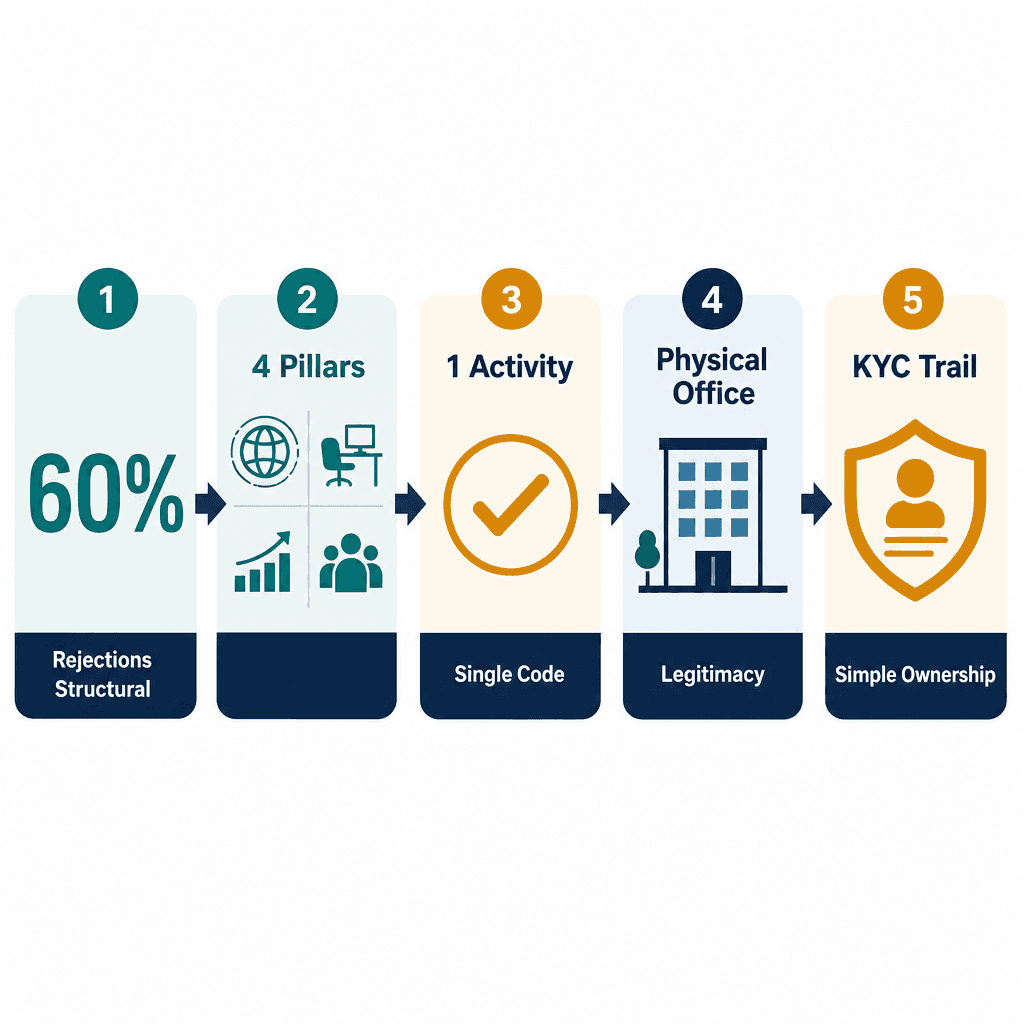

The most common complaint from UAE free zone company owners is straightforward: they can't open a bank account. More than 60% of rejections, based on practitioner experience across hundreds of applications, trace back not to bank policy but to preventable structural problems, the wrong free zone, the wrong office type, a vague business activity, or a shareholder profile that triggers enhanced due diligence. The bank isn't the obstacle. The company structure is.

This guide breaks down the exact free zone company structure decisions, from free zone selection and office type to shareholder profile and business activity, that determine whether a UAE bank says yes or no. If you're planning a UAE free zone company and banking is a priority, read this before you incorporate, not after your first rejection.

What Is Free Zone Company Structure for Easy Bank Account Opening in UAE and Why It Matters

A free zone company structure for easy bank account opening in UAE refers to the deliberate combination of free zone choice, office solution, business activity, and shareholder profile that satisfies UAE bank compliance requirements. Getting these four elements right from incorporation dramatically reduces the risk of account rejection.

Why Most Rejections Are a Structure Problem, Not a Bank Problem

UAE banks aren't arbitrarily difficult. They operate under strict UAE Central Bank AML and KYC frameworks that make certain company profiles high-risk by default. A compliance officer reviewing your application doesn't have discretion to ignore red flags, the framework requires them to act on what they see.

The most common rejection triggers are structural, not personal:

Vague or dual business activities (e.g. "general trading and investment advisory")

Virtual office address with no verifiable physical presence

Non-resident shareholders from high-scrutiny jurisdictions

No trading history or transaction purpose at time of application

Framing the issue correctly saves months of wasted effort. One consultant incorporated in a newer offshore-adjacent free zone, listed a virtual office address, and registered both "general trading" and "investment advisory" as co-equal activities. Three banks rejected the application. After restructuring to a single professional services activity with a flexi desk at Dubai South Business Hub (DSBH), the account was approved within three weeks. The company hadn't changed. The structure had. For more on what triggers rejections, see why your UAE business bank account was rejected.

The Four Structural Pillars Banks Evaluate Before Saying Yes

Every UAE bank compliance review, whether you're applying at Emirates NBD, RAKBank, or Mashreq, assesses the same four pillars: free zone credibility, office solution, business activity clarity, and shareholder profile. Weakness in any one pillar raises scrutiny across the others.

DMCC, DAFZA, JAFZA, and DSBH are consistently cited by UAE relationship bankers as free zones they're comfortable onboarding. DMCC alone hosts over 23,000 member companies (DMCC, 2025), making it one of the most bank-recognised free zones globally. The UAE has over 45 free zones in total, but bank familiarity varies enormously across them. Newer, offshore-adjacent, or lightly regulated free zones carry higher compliance friction regardless of their legal legitimacy.

Which Free Zone You Choose Determines Whether the Bank Says Yes

For the best free zone for banking in UAE, DMCC, DAFZA, JAFZA, and Dubai South Business Hub are the most bank-recognised options. These free zones have established compliance reputations and direct relationships with major UAE banks, making the free zone company structure bank account UAE process significantly more predictable.

Bank-Recognised Free Zones vs. High-Friction Free Zones

UAE banks informally tier free zones by compliance track record and regulatory oversight quality. Here's how the top four break down by sector and banking relationship strength:

DMCC, commodities, trading, professional services; strong global name recognition and long-standing relationships with major UAE banks

DAFZA, aviation, logistics, technology; preferred by banks for import/export and professional service companies operating internationally

JAFZA, manufacturing, logistics, large-scale trading; backed by DP World, well-understood by trade finance desks at Emirates NBD and Abu Dhabi Commercial Bank

DSBH, aviation, logistics, e-commerce, professional services; on-site banking partnerships with RAKBank and Mashreq that no other free zone in this list replicates

A logistics company that incorporated at JAFZA reported same-day preliminary approval from Emirates NBD's trade finance team. The bank had a dedicated JAFZA onboarding desk, a relationship built over decades of processing JAFZA client applications. That's the kind of institutional familiarity that translates directly into faster decisions.

How DSBH's On-Site Banking Partnerships Change the Equation

Dubai South Business Hub has formalised banking partnerships with RAKBank business banking at Dubai South and Mashreq corporate banking at Dubai South. Account managers are physically present or regularly accessible within the free zone itself. That removes the cold-outreach problem entirely.

A DSBH-licensed e-commerce company used the on-site Mashreq relationship to open a multi-currency account within 15 business days. The same founder had previously spent over three months attempting to open an account at a non-partner bank from a different free zone. The free zone changed. The banking timeline changed dramatically. For a full picture of what DSBH offers on the banking side, see DSBH banking and taxation services.

Seven Structural Decisions That Make UAE Bank Account Opening Straightforward

To set up a company for easy banking in the UAE, seven decisions need to be made correctly: choose a bank-recognised free zone, take a flexi desk or physical office, select a single clear business activity, keep the shareholder structure simple, prepare a one-page company description, approach the right bank, and time your application when your first invoice is ready.

Decisions One Through Four: Structure, Space, Activity, and Ownership

Free zone selection: Choose DMCC, DAFZA, JAFZA, or DSBH for maximum bank recognition. Before incorporating, confirm whether your target bank has an existing relationship with your chosen free zone. This one step eliminates a significant portion of avoidable friction.

Office solution: Virtual offices are the most common rejection trigger after vague activity. A flexi desk is acceptable to most UAE banks as evidence of operational presence. A physical office is the gold standard and removes compliance scrutiny about whether your business is genuinely operating.

Business activity clarity: Single, well-defined activities, management consulting, freight forwarding, software development, are straightforward for compliance teams to underwrite. Avoid combining financial intermediation, money services, or cryptocurrency with other activities unless you have the regulatory licenses and compliance infrastructure to justify them.

Shareholder profile: UAE-resident shareholders are preferred. Non-resident shareholders aren't disqualifying, but they require certified passport copies, proof of address, source of funds documentation, and sometimes a video KYC call. Multi-jurisdiction holding structures with intermediate SPVs trigger beneficial ownership tracing requirements under UAE UBO regulations, each additional layer adds weeks.

A US-based founder who initially listed "general trading, financial consultancy, and digital assets" as three co-equal activities was advised to narrow to a single activity, "management consultancy", before reapplying. Mashreq approved the revised application in under three weeks. The business hadn't changed. The activity description had.

Office Solution Comparison: Virtual Office vs Flexi Desk vs Physical Office for UAE Bank Account Opening

Feature | Physical Office | Flexi Desk | Virtual Office |

|---|---|---|---|

Bank Acceptance Rate | ✅ Highest, removes all presence-related queries | ✅ Accepted by most UAE banks | ❌ Frequently flagged as a risk indicator |

Physical Verifiability | ✅ Fully verifiable; dedicated lease on record | ✅ Verifiable shared workspace address | ❌ Mailing address only; no physical verification possible |

Compliance Signal Sent | Strong operational legitimacy signal | Adequate operational presence signal | Raises AML/KYC concern about real operations |

Typical Cost Level | AED 30,000+ per year (dedicated lease) | AED 8,000–15,000 per year | AED 1,500–5,000 per year |

Recommended For | Trading companies, firms with staff, credit facility applicants | Service businesses, consultants, small e-commerce teams | Not recommended if UAE bank account is required |

Available at DSBH | ✅ Yes | ✅ Yes | ❌ Not the recommended entry point |

Decisions Five Through Seven: Documentation, Bank Choice, and Timing

Company description document: A clear one-page overview explaining what the business does, who its customers are, where revenue comes from, and what the expected monthly transaction volume looks like. This single document answers the majority of banker queries before they become formal information requests, and it signals that you understand your own business well enough to explain it clearly.

Bank selection: Approach banks with a known relationship with your free zone. Cold-approaching a bank that has never processed an application from your free zone requires their compliance team to evaluate the free zone itself from scratch, adding weeks to your timeline. Use your free zone's banking partnerships where they exist. See how to open a corporate bank account in Dubai for a step-by-step breakdown.

Timing: Apply when your first invoice is ready, not before. Banks assess "purpose of account" as a mandatory KYC field. A dormant company with no imminent trading activity is harder to onboard than one with a signed contract or a pro-forma invoice already issued.

A DSBH freight forwarding company waited until it had both a signed customer agreement and a pro-forma invoice before approaching RAKBank on-site. The relationship manager described it as one of the cleanest applications the team had processed. Approval came in 10 business days.

Free Zone Office Solutions and How They Affect Your Bank Application

For UAE bank account applications, a physical office is the strongest signal of operational legitimacy, a flexi desk is acceptable to most banks, and a virtual office is the most common structural trigger for rejection. The office solution you choose at incorporation directly affects how a bank's compliance team assesses your company structure for bank account Dubai purposes.

Virtual Office, Flexi Desk, or Physical Office: What Each Signals to a Banker

A virtual office gives you a mailing address with no physical presence. UAE banks flag these as a risk indicator because their compliance teams can't verify that a real business is operating at the address. The Central Bank's AML framework requires banks to assess operational legitimacy, a PO box equivalent doesn't satisfy that requirement.

A flexi desk is a shared workspace with a designated desk and a verifiable address. Most UAE banks accept this as adequate evidence of operational presence. It's cost-effective and entirely appropriate for service businesses, consultants, and small e-commerce teams. A physical office, a dedicated leased space with your company's name on the door, is the strongest compliance signal available and is recommended for trading companies, businesses with staff, or any company planning to apply for credit facilities alongside a current account.

DSBH offers both flexi desk and physical office options within the free zone. Its on-site banking partners, RAKBank and Mashreq, are already familiar with both address types. That means your address is immediately recognisable and verifiable to the compliance team, no additional site visits, no requests for third-party verification letters.

What to Keep in Mind Before Choosing Your Office Solution

The office decision is often made on cost alone. That's a mistake if banking is a priority. A company structure for bank account Dubai purposes needs to treat the office solution as a compliance decision first and a cost decision second. Saving AED 10,000 on a virtual office package can cost months of application time and multiple rejection cycles.

Some free zones offer only virtual office solutions at entry-level price points. If you're comparing free zones and one of them only offers a virtual address at incorporation, factor in the banking friction that creates from day one. DMCC, DAFZA, JAFZA, and DSBH all offer flexi desk and physical office options that are bank-compliant.

Shareholder Profile and Business Activity: The Two Factors Banks Scrutinise Most

UAE banks conduct enhanced due diligence on companies with non-resident shareholders, multi-jurisdiction ownership structures, or high-risk business activities such as financial intermediation or cryptocurrency. Keeping your free zone company structure bank account UAE setup simple on both fronts dramatically reduces compliance friction.

Shareholder Residency and Ownership Structures That Raise Compliance Flags

UAE-resident shareholders are preferred by banks because Emirates ID, visa status, and local identity verification provide a clear, auditable KYC trail. Non-resident shareholders aren't disqualifying, but they require certified passport copies, proof of address, source of funds documentation, and sometimes a video KYC call. Each additional requirement extends the timeline by days or weeks.

Multi-jurisdiction holding structures are the most significant timeline risk. A UAE free zone company owned by a BVI holding company, which is in turn owned by a Cayman trust held by a family office, triggers beneficial ownership tracing requirements under UAE UBO regulations. Banks must verify every layer before approval. A European family office that owned a DMCC subsidiary through two intermediate holding companies in Luxembourg and the BVI waited four months for bank approval, not because the structure was illegal, but because the bank had to complete UBO verification at each layer. UAE UBO regulations require disclosure of all beneficial owners holding 25% or more (UAE Cabinet Decision No. 58 of 2020, still accurate as of 2026). The simplest structure that works: direct individual ownership, UAE residency, single class of shares, no intermediate entities unless operationally essential.

Worth flagging: the FATF removed the UAE from its grey list in 2024 after placing it there in 2022 (FATF, 2024). UAE banks responded to the grey-listing period by tightening AML standards significantly, those standards remain in place even after removal. Applications that would have passed in 2021 may now require additional documentation.

Choosing a Business Activity That Banks Understand and Accept

Low-friction activities, management consulting, IT services, freight forwarding, import/export of specific goods, e-commerce, have clear transaction flows and are straightforward for compliance teams to assess. High-friction activities, financial intermediation, money exchange, payment services, cryptocurrency trading, precious metals, require detailed justification and sometimes separate regulatory licenses. They trigger enhanced due diligence regardless of which free zone you're in.

Does listing multiple activities on a UAE free zone license hurt your bank application?

Yes, in most cases. UAE free zone licenses can carry multiple activities, but banks prefer applic

References

Editorial sources available on request. Full citation list is being compiled.