Topic Summary

By Editorial Team , UAE business setup specialists with direct experience guiding investor visa holders through free zone company formation and residency compliance. Full bio →

Last updated: June 2026

By Editorial Team, UAE business setup specialists with direct experience guiding investor visa holders through free zone company formation and residency compliance. Full bio →

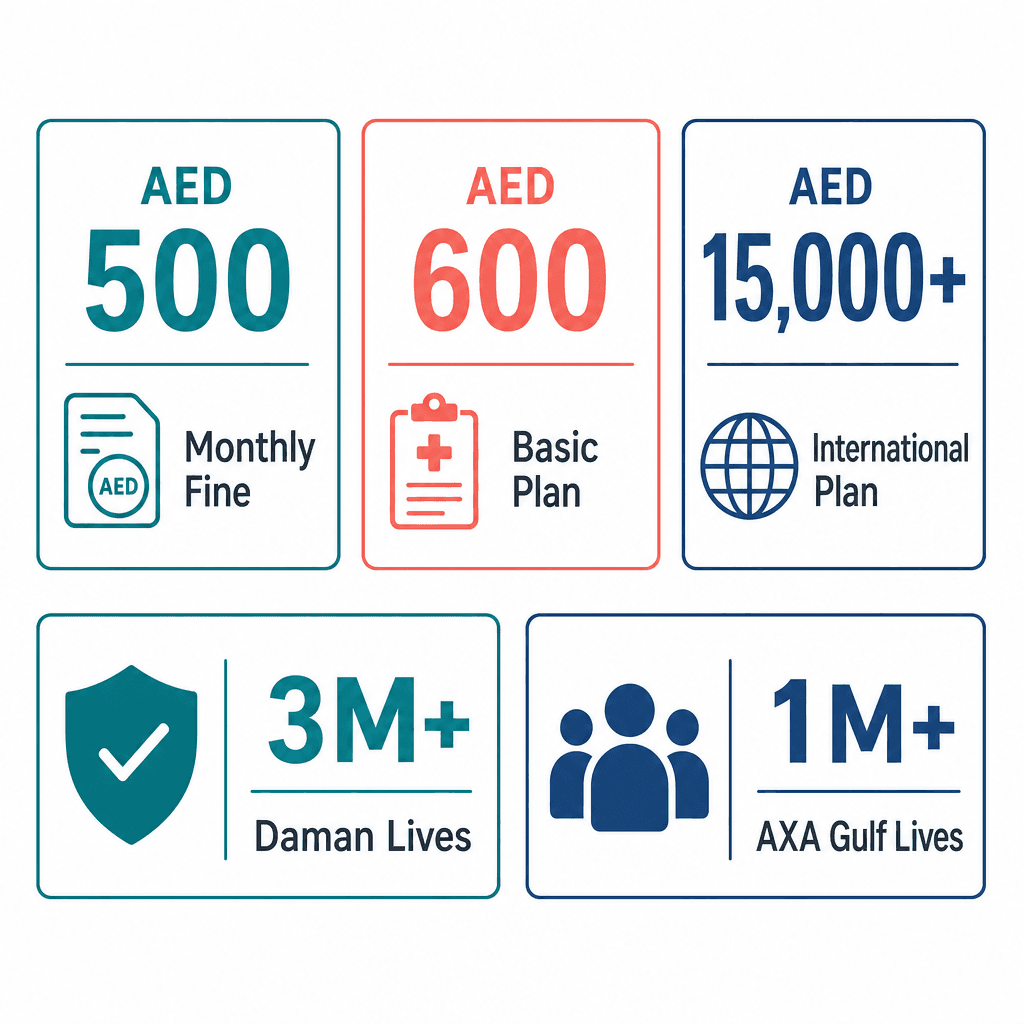

In 2026, every UAE resident, including investors, sole traders, and company directors, must hold valid health insurance, with non-compliance penalties reaching AED 500 per month per uninsured individual in Dubai alone (Dubai Health Authority, 2024). The UAE's mandatory insurance framework covers all visa holders: employees, dependants, and business owners alike. Premiums for an enhanced individual plan start at AED 2,000 per year (DHA network data, 2025). Basic Essential Benefits Plan coverage costs as little as AED 600 per year, while international plans can exceed AED 15,000 annually. Daman, Abu Dhabi's government-backed insurer, administers cover for over 3 million Abu Dhabi residents (Daman, 2023). And AXA Gulf serves over 1 million lives across the UAE (AXA Gulf, 2023).

Here's the thing most new business owners miss: if you run your own company in the UAE, you're both the employer and the employee. That means sourcing your own health insurance for business owners in the UAE, at the right level, from the right provider, with no HR team handling it for you. This guide covers the mandatory framework, the three plan tiers, the leading insurers, what you specifically need to consider as an entrepreneur, typical costs in AED, and a step-by-step comparison method so you can choose with confidence.

What Is the Mandatory Health Insurance Obligation for UAE Residents

Health insurance is legally mandatory for all UAE residents. In Dubai, the Health Insurance Law requires all employers, including business owners, to provide cover for themselves and any staff. Abu Dhabi operates its own scheme under Daman. Failure to comply attracts monthly fines per uninsured individual. For health insurance for business owners in the UAE, this is non-negotiable: the obligation kicks in at the visa stage and is enforced at every renewal.

Dubai's Health Insurance Law and What It Means for You

The Dubai Health Authority enforces mandatory health insurance under Law No. 11 of 2013. The law covers all Dubai residents without exception: employees, dependants, and investor or partner visa holders. If you're a business owner on an investor visa, your company is technically your employer, which means your company must provide your insurance, and you're the one arranging it.

The penalty for non-compliance is AED 500 per month per uninsured individual, applied at visa renewal (DHA, 2024). That means a sole-director free zone company at Dubai South with zero employees still has one person to insure: the director. That obligation falls entirely on the business owner, not a payroll department.

Governing legislation: Law No. 11 of 2013 (Dubai Health Insurance Law)

Enforcing authority: Dubai Health Authority (DHA)

Non-compliance penalty: AED 500 per month per uninsured person

Scope: all Dubai visa holders, including investor and partner visa Dubai holders

How Abu Dhabi's Scheme Differs from Dubai's

Abu Dhabi runs its own mandatory health insurance system through Daman (the National Health Insurance Company), and it predates Dubai's law by several years. Emirati nationals in Abu Dhabi are covered under the government's Thiqa programme. Expatriate residents, including business owners on investor visas, must hold a valid Daman-approved policy. The Abu Dhabi Department of Health oversees compliance.

The two systems are not interchangeable. An entrepreneur who relocates from a Dubai free zone to an Abu Dhabi mainland entity must switch to a Daman-approved provider. A Dubai-issued policy won't satisfy Abu Dhabi's Department of Health requirements, even if it's from a nationally recognised insurer. Check your emirate of visa issuance before selecting any plan.

Types of Health Insurance Plans Available to Business Owners in the UAE

UAE health insurance plans fall into three main tiers: the basic DHA-mandated plan covering essential inpatient care, enhanced plans adding wider networks and outpatient cover, and international plans providing worldwide coverage including the UAE. For health insurance for business owners in the UAE and medical insurance for entrepreneurs in Dubai, the enhanced tier is typically the practical minimum, not the basic plan.

Basic DHA-Mandated Plans, the Legal Minimum

The Essential Benefits Plan (EBP) is the DHA's minimum-coverage product, designed for employees earning under AED 4,000 per month. It covers inpatient care, emergency treatment, and basic diagnostics within a defined DHA network. Annual premiums run AED 600–1,500, making it the cheapest option on paper.

But here's the catch: the EBP network is restricted to DHA-approved clinics serving lower-income brackets. A construction company owner who selects an EBP for themselves may find that a specialist consultation at a private hospital in Dubai Marina is completely out-of-network, meaning full out-of-pocket cost. For most business owners, the EBP is a compliance floor, not a practical choice.

Enhanced Plans, the Practical Choice for Most Entrepreneurs

Enhanced or standard plans expand the hospital network to major private providers, Mediclinic, American Hospital Dubai, Cleveland Clinic Abu Dhabi, and typically include outpatient GP visits, specialist referrals, pharmacy cover, and optional dental or optical riders. Annual premiums range from AED 2,000–5,000 depending on age, health profile, and chosen network tier.

A 38-year-old entrepreneur based near Dubai South paying AED 3,200 per year on a standard AXA Gulf plan gains access to over 1,000 in-network providers, including outpatient GP visits and up to AED 1,500 dental cover. That's the kind of access most business owners actually need. Key inclusions to look for:

Outpatient consultations (GP and specialist)

Pharmacy cover up to an annual limit

Diagnostic tests and imaging

Optional dental rider (AED 400–800/year additional)

Optional optical rider for glasses or contact lenses

International Health Insurance Plans, for Globally Mobile Owners

International Private Medical Insurance (IPMI) plans cover the holder worldwide, including the UAE. They suit entrepreneurs who travel frequently or split time between the UAE and Europe, North America, or Asia. Providers include MSH International, Bupa Global, and AXA International, with annual premiums from AED 6,000 to AED 15,000 or more.

A British entrepreneur running a consultancy from Dubai but spending three months per year in Europe can select an MSH International plan covering both regions under a single policy, removing the need for separate travel health cover. Worth flagging: not all international plans satisfy DHA or Abu Dhabi Department of Health mandatory insurance requirements. Always confirm compliance before purchasing.

Key Insurers Offering Private Health Insurance UAE, and How They Compare

The main providers of private health insurance in the UAE are Daman, AXA Gulf, Bupa Arabia, MetLife, Orient Insurance, and MSH International. Each differs on network size, premium levels, claims processing speed, and international reach. For the best health insurance for Dubai self-employed founders, the right comparison axis is network fit and outpatient terms, not headline premium.

Daman, AXA Gulf, and Bupa Arabia, the Tier-One Providers

Daman: Abu Dhabi's government-backed insurer. Dominant in the capital, required for Abu Dhabi visa holders. Strong network and consistent claims handling.

AXA Gulf: One of the largest private insurers in the UAE, serving over 1 million lives (AXA Gulf, 2023). Broad Dubai network, competitive SME and individual plans, fast claims processing.

Bupa Arabia: Strong in individual and family plans, competitive on outpatient limits, well-regarded for chronic condition management.

An entrepreneur relocating from Abu Dhabi to Dubai who switches from Daman to AXA Gulf will find comparable network access in Dubai. But they should recheck that their preferred specialist clinic accepts the new insurer before finalising the switch. Network lists change annually, and a clinic that was in-network last year may not be this year.

MetLife, Orient Insurance, and MSH International, Alternatives Worth Considering

MetLife UAE: Strong life-and-health bundle options. Suits business owners wanting combined life and medical cover under one provider.

Orient Insurance: Competitive pricing on individual plans, solid Dubai network. Often undercuts larger providers on standard tiers.

MSH International: Specialist in expat and internationally mobile cover. Ideal for entrepreneurs splitting time between the UAE and overseas.

Pre-existing condition exclusion periods range from 6 to 36 months depending on insurer and plan tier. A 45-year-old entrepreneur with a managed pre-existing condition found Orient Insurance's 24-month exclusion period meaningfully shorter than a competitor's 36-month window, a real difference in practical terms. Dubai South and other free zones don't mandate a specific insurer; you can select any DHA-approved provider from the list published by the Dubai Health Authority.

UAE Health Insurers Compared, Key Criteria for Business Owners

Feature | AXA Gulf / Bupa Arabia | Orient / MetLife / MSH |

|---|---|---|

Dubai Network Size | ✅ 1,000+ in-network providers | ✅ Solid; varies by tier |

Abu Dhabi Coverage | ✅ Strong (Daman-linked) | ⚠️ Verify per plan |

Individual Plan Premium (Enhanced) | AED 2,500–5,000/yr | AED 2,000–4,500/yr |

International Coverage | ❌ UAE-focused (standard plans) | ✅ MSH covers worldwide |

Pre-Existing Exclusion Period | 12–24 months (Bupa Arabia) | 24–36 months (varies) |

Life + Health Bundle | ❌ Separate products | ✅ MetLife bundles available |

Best For | UAE-based entrepreneurs, families | Mobile founders, budget-conscious |

What Business Owners Specifically Need to Consider When Choosing Medical Insurance

Medical insurance for entrepreneurs in Dubai and health insurance for free zone company owners in the UAE involves decisions that salaried employees simply don't face. You fund the premium entirely yourself. Your premium reflects your personal age and health profile, not a group rate. And your visa type, investor or partner, determines which plans you can access. There's no HR team managing renewals.

You're Covering Yourself on an Investor or Partner Visa

Business owners in UAE free zones or on mainland typically hold investor visas or partner visa Dubai, not employment visas. Your company is legally the sponsoring employer, which means your company must provide your insurance. In practice, that means you choose the plan and pay the premium directly.

Your policy is individually underwritten. Age, gender, and health history all affect pricing. A 50-year-old business owner on a partner visa will pay materially more than a 32-year-old on an identical plan, with age banding typically increasing premiums by 20–40% per decade above 40. Factor this into your cost of running a business in Dubai projections from day one.

Covering Dependants and Employees as Your Business Grows

If you sponsor family members on your company visa, you must provide them with health insurance too. Every employee you add triggers the same mandatory insurance obligation. Group plans become available once you reach three or more covered lives, and they typically reduce per-head premiums by 10–25% compared to individual plans.

A free zone company at Dubai South with a founder, two employees, and one sponsored spouse needs four separate insurance certificates. A group plan arranged through a benefits platform like Bayzat, available through HR and employee benefits management at Dubai South, handles all four in one place, including renewals and compliance tracking.

Is health insurance tax-deductible for UAE business owners?

Under the UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022), health insurance premiums paid by a business for its employees and directors are generally deductible as a business expense, provided they are incurred wholly and exclusively for business purposes. Confirm with a UAE-registered tax agent for your specific structure.

How to Compare Health Insurance Plans in the UAE: a Step-by-Step Guide

To compare UAE health insurance plans effectively, check hospital network coverage in your area, outpatient consultation limits, dental and optical inclusions, pre-existing condition exclusion periods, annual coverage limits, and claims processing reputation. Price alone is a poor guide for health insurance for business owners in the UAE, network fit and outpatient access matter more for the best health insurance for Dubai self-employed individuals.

Step 1: Verify the Hospital Network Covers Your Location

Every insurer publishes a network list. Check your nearest hospital and preferred specialist clinic are included before you look at premiums. Network tiers matter: premium or flexi networks include top-tier private hospitals, while standard networks may exclude them entirely.

Dubai and Abu Dhabi have separate networks, check coverage in each if you operate across both emirates

Out-of-network treatment typically costs 3–5 times more than in-network rates

An entrepreneur based near Dubai South should confirm Al Maktoum Hospital is in-network before selecting a plan, not all standard plans include it

Step 2: Assess Outpatient Limits, Dental Cover, and Optical Riders

Outpatient limits cap how much the insurer covers for GP visits, specialist consultations, and diagnostics per year. Dental cover is rarely included as standard, it's a paid rider costing AED 400–800 per year extra. Optical cover for glasses or contact lenses is similarly an add-on.

A self-employed consultant who sees a GP monthly and a specialist quarterly should calculate expected outpatient spend before choosing a plan. A AED 500/year saving on premium can be wiped out by a single uncovered specialist visit. Outpatient limits range from AED 5,000 to unlimited depending on plan tier, this is the number to compare, not just the headline premium.

Step 3: Read the Pre-Existing Condition Exclusion Terms Carefully

Most UAE insurers apply a waiting period for pre-existing conditions: typically 6–36 months before claims are accepted. Chronic conditions like diabetes or hypertension may be permanently excluded on standard plans. Non-disclosure of a condition is grounds for claim rejection or full policy cancellation, declare everything accurately.

A business owner with managed hypertension found that Bupa Arabia's 12-month exclusion period on their standard plan was half the 24-month window offered by a cheaper competitor. That difference made the slightly higher premium worthwhile. On group plans, shorter exclusion periods are sometimes negotiable, worth asking.

Typical Health Insurance Costs in the UAE for Business Owners

Health insurance costs in the UAE for business owners range from AED 600–1,500 per year for a basic DHA plan, AED 2,000–5,000 for an enhanced plan, and AED 6,000–15,000 or

References

Editorial sources available on request. Full citation list is being compiled.